DeFi Lending 101: Understanding Liquidation & LTV

Learn how DeFi lending works on Aave, understand Loan-to-Value (LTV), and discover the critical steps to avoid crypto asset liquidation. Borrow safely with these insights.

Welcome to Article 27 in our Web3 101 series. Today, we're tackling one of DeFi's most powerful, yet riskiest, sectors: Lending & Borrowing. We will break down how you can borrow assets without KYC and, more importantly, how to avoid the catastrophic event known as liquidation.

Imagine needing cash but not wanting to sell your precious ETH or BTC, especially when you believe they will appreciate. In traditional finance, this would involve paperwork, credit checks, and a lengthy approval process. In Web3, you can get a loan in minutes using your crypto as collateral. But this power comes with a critical risk that every newcomer must understand: liquidation.

What is DeFi Lending & Borrowing?

At its core, DeFi lending allows users to lend their crypto assets to earn interest or borrow assets against collateral. Instead of banks, these transactions are handled by smart contracts on platforms like Aave, Compound, or Radiant. These protocols operate on a pool-based model: lenders deposit their assets into a large liquidity pool, and borrowers can draw from this pool.

The entire process is permissionless. As long as you have a non-custodial wallet and some crypto, you can participate. This is where the Coin98 Super Wallet becomes your gateway. Through our integrated DApp Browser, you can connect to these lending platforms securely, ensuring you are interacting with the official smart contracts and not a phishing site.

The Core Mechanics: Over-Collateralization and LTV

Since there's no KYC or credit score, how do these protocols trust you'll repay your loan? They don't have to. The system is built on a trustless foundation secured by two key concepts.

Over-Collateralization: The DeFi Safety Net

Over-collateralization is the fundamental principle of DeFi lending. It means you must deposit collateral that is worth significantly more than the amount you want to borrow. For example, to borrow $700 worth of USDC, you might need to deposit $1,000 worth of ETH.

This extra collateral acts as a buffer against market volatility. If the price of your collateral (ETH) starts to drop, the protocol still has a cushion to ensure the loan can be repaid, protecting the funds of the lenders.

LTV (Loan-to-Value): The Most Important Metric to Watch

So, how much can you borrow against your collateral? This is determined by the LTV, or Loan-to-Value ratio. It's the most critical metric you need to monitor.

- Definition: LTV represents the ratio of your loan's value to your collateral's value.

- Formula: LTV = (Loan Amount / Collateral Value) * 100%

Each asset on a platform like Aave has a specific 'Maximum LTV'. For a stable asset like ETH, the max LTV might be 75%. For a more volatile altcoin, it could be as low as 40%. This means with $1,000 of ETH, you can borrow a maximum of $750. With $1,000 of a riskier asset, you might only be able to borrow $400.

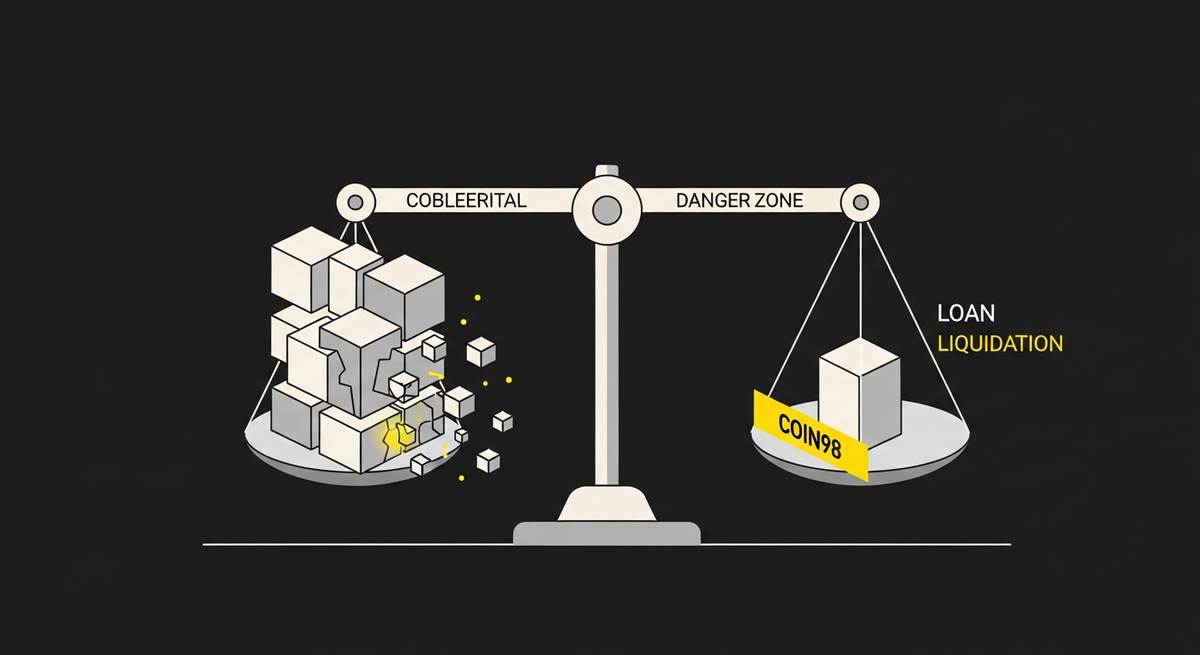

The Danger Zone: Understanding Liquidation

This is where the real risk lies. If the market turns against you and the value of your collateral drops, your LTV will rise. If it crosses a certain point, your position is automatically closed.

What is Crypto Asset Liquidation?

Liquidation is the forceful, automated sale of your collateral by the protocol to repay your loan. This happens when your LTV ratio exceeds a predefined 'Liquidation Threshold' (e.g., 80%). This is not a request; it's a smart contract function that executes automatically to keep the protocol solvent.

A Step-by-Step Liquidation Scenario

Let's walk through an example:

- Deposit: You deposit 10 ETH, currently worth $20,000, into Aave.

- Borrow: The Liquidation Threshold for ETH is 82.5%. You decide to be safe and borrow $10,000 USDC. Your initial LTV is 50% ($10,000 / $20,000).

- Market Crash: The crypto market experiences a sharp downturn. The price of ETH drops 35%, and your collateral is now only worth $13,000.

- LTV Spike: Your loan is still $10,000, but your collateral has shrunk. Your new LTV is now approximately 76.9% ($10,000 / $13,000). You are getting close to the threshold.

- Liquidation Trigger: The price of ETH drops further. Your collateral is now worth $12,000. Your LTV hits 83.3% ($10,000 / $12,000), crossing the 82.5% threshold.

- The Result: The protocol seizes a portion of your ETH collateral and sells it on the open market to repay your $10,000 USDC loan. You lose that portion of your ETH forever.

The Liquidation Penalty: Adding Insult to Injury

To make matters worse, protocols charge a liquidation penalty (or fee). This fee, often between 5-10% of your loan value, is given to the 'liquidator' (a bot or user who executes the liquidation) as an incentive. This means you not only lose your collateral but also pay an extra penalty on top.

How to Avoid Liquidation: Proactive Strategies

Managing a DeFi loan is not a set-it-and-forget-it activity. Here’s how our team at Coin98 suggests you protect yourself:

- Maintain a Healthy LTV: Never borrow the maximum amount. A conservative LTV of 30-40% gives you a much larger buffer to withstand market volatility.

- Set Up Alerts: Manually tracking asset prices is stressful and impractical. Within the Coin98 Super Wallet, you can use the 'Price Alerts' feature. Set an alert for when your collateral asset (like ETH) drops to a certain price. This gives you an early warning to take action before your position becomes critical.

- Be Prepared to Act: Have extra assets readily available in your wallet. If you receive a price alert, you can quickly open the DApp browser, connect to the lending protocol, and either:

1. Add more collateral to lower your LTV.

2. Repay a portion of your loan, which also lowers your LTV. - Use Stablecoins as Collateral: If you want to borrow a volatile asset, consider using stablecoins (USDC, USDT) as collateral. Since their value doesn't fluctuate, the risk of liquidation is virtually zero.

Conclusion: Borrow Smart, Not Hard

DeFi lending offers incredible opportunities for capital efficiency, but it demands respect for its inherent risks. Understanding over-collateralization, diligently monitoring your LTV, and having a plan to avoid liquidation are not optional—they are essential for survival. By using the right tools and strategies, you can leverage this powerful DeFi primitive without getting burned.

Ready to explore DeFi lending safely? Download the Coin98 Super Wallet today to manage your portfolio, set crucial price alerts, and interact with top lending DApps seamlessly. Your journey into smarter DeFi starts here.

Frequently Asked Questions (FAQ)

What is liquidation in DeFi lending?

Liquidation is the automated process where a lending protocol sells your collateral to repay your loan if its value drops and your Loan-to-Value (LTV) ratio exceeds a set threshold.

What does LTV mean in crypto?

LTV, or Loan-to-Value, is the ratio of your borrowed amount against the current market value of your collateral. It's a key metric for assessing the risk of your loan.

How can I avoid liquidation?

To avoid liquidation, maintain a low LTV, borrow less than the maximum allowed, set price alerts for your collateral, and be prepared to add more collateral or repay your loan during market downturns.

What is over-collateralization?

Over-collateralization means you must deposit collateral that is worth more than the amount you wish to borrow. This acts as a safety buffer for the lender against price volatility.